Executive Summary

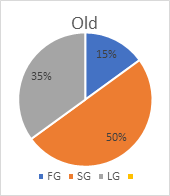

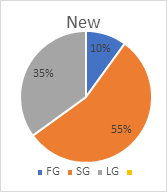

Nigeria has introduced a new Value Added Tax (VAT) revenue sharing formula as part of its broader tax reforms aimed at improving fiscal federalism and strengthening the finances of state governments. Under the revised structure, the Federal Government now receives 10% of VAT revenue, states receive 55%, and local governments receive 35%, replacing the previous formula of 15%, 50%, and 35% respectively as shown below. The change shifts a larger share of VAT revenue to subnational governments and is expected to significantly increase the funds available to states for development and public services.

Background

Value Added Tax (VAT) is one of Nigeria’s major non-oil revenue sources. It is a consumption tax charged on goods and services and is collected centrally by the Federal Government through the tax authority before being distributed among the three tiers of government.

Historically, VAT revenue has been shared using a vertical allocation formula that determines how the total VAT pool is distributed among the Federal Government, state governments, and local governments. The previous formula allocated 15% to the Federal Government, 50% to states, and 35% to local governments.

However, ongoing debates about fiscal autonomy and fair distribution of resources led to reforms in Nigeria’s tax laws and a revision of the VAT sharing framework.

Key Changes in the New VAT Sharing Formula

1. Revised Allocation Among the Three Tiers of Government

| OLD | NEW | |

| Federal Government | 15% | 10% |

| State Government | 50% | 55% |

| Local Government | 35% | 35% |

| Total | 100% | 100% |

This represents a five-percentage-point reduction in the Federal Government’s share and a corresponding increase in the share allocated to states.

2. Increased Revenue for States

The revised structure is expected to increase revenue for state governments. Estimates suggest that states could collectively receive over ₦5 trillion annually from VAT allocations under the new framework.

3. Distribution To the States

Once VAT revenue is aggregated, it is further distributed to the states using internal criteria such as:

- Equality among states

- Population size

- Consumption or derivation factors

These principles are designed to ensure that revenue allocation reflects both economic activity and demographic factors across the country.

Conclusion

Nigeria’s revised VAT sharing formula marks a significant shift in the country’s tax administration and fiscal structure. By increasing the share of VAT revenue allocated to states, the reform aims to strengthen subnational finances and promote more balanced economic development across the federation. As Nigeria continues to implement broader tax reforms, the effectiveness of the new VAT distribution system will depend on transparent administration, equitable allocation, and responsible use of the additional revenue by states and local governments.

References

- Africa Check. Factsheet: VAT and Income Tax in Nigeria’s New Tax Rules.

- The Cable. FAAC Allocation Under New VAT Sharing Formula.

- Punch Nigeria. Tax Law: VAT Hits Record ₦1tn as New Sharing Era Begins.

- Punch Nigeria. N5tn VAT Windfall for States as New Formula Begins

Leave A Comment